The Home button at the end of each topic takes you to the Home page.

The Menu button provides access to the individual topics.

The Resources button provides a list of useful links.

The Switch Language button lets you switch to a different language.

The Close button ends your training session and closes the course window.

Citi’s culture and values are at the heart of how business is conducted. A strong risk and control environment is a key enabler of Citi’s culture of excellence.

This intermediate course is part of Citi’s Enterprise Risk Management Training Program (ERMTP). ERMTP is a series of courses which will build your understanding of your risk and control responsibilities.

Citi has a standard framework for managing risk. As part of Citi's Enterprise Risk Management Framework (ERMF) supporting capabilities, we are committed to equipping employees with knowledge to carry out day-to-day risk and control responsibilities.

Managing risk is everyone’s job at Citi. We are all risk managers. Risk is inherent to Citi’s business and cannot be avoided. Everyone must be vigilant and manage risk with consistency, and accountability including compliance with applicable laws and regulations.

The Enterprise Risk Management Framework (ERMF) is Citi’s standard for managing risk.

Everyone is responsible for escalating risks and concerns, and Citi provides an environment where this can be done without fear of retribution.

It is your responsibility to understand your role as it relates to managing risk, taking complete ownership of your actions, and supporting Citi in identifying and managing risk every day.

Fairness

Must be fair to customers and meet their needs. Fairness considers customer debt leverage, value to the customer and avoidance of predatory practices.

Strategic Alignment

Align product purpose, value proposition and credit policy.

Underwriting Focus

More underwriting scrutiny to determine ability to pay applies to customers without credit experience or significant negative history without compensating factors.

Payment for Risk

Citi must get paid for the risk it takes.

A Risk Readiness Playbook (RRP) is a portfolio-level, forward-looking Retail risk management tool that triggers appropriate risk mitigating activities when defined leading indicators are tripped.

Detailed requirements for RRPs are outlined in the RCR Credit Performance Management Standard.

To proceed, select each aspect to find out what an RRP involves.

Risks

Identifying and evaluating relevant portfolio risk and external drivers and/or adverse scenarios.

Triggers

Setting appropriate triggers to prompt closer attention to heightened risk.

Plans

Creating corresponding action plans to minimize the anticipated adverse impact.

Benchmarks are credit quality measures that outline expected portfolio performance at specific points in time and must be in place for any Retail portfolio actively extending credit via new account acquisition or ECM actions. Benchmarks require re-validation and approval at least annually.

For a deeper dive into benchmarks, consider the frequently asked questions below and refer to the RCR Credit Performance Management Standard.

Why are benchmarks important?

As one of the fundamental methods for managing credit risk, portfolio performance against benchmarks is monitored frequently to determine if the portfolio is performing as expected or if any breaches to a benchmark occurred. Tracking against benchmarks is included in PRAP and PQR/CRO reviews for on-going portfolio monitoring.

What do acquisition benchmarks include?

Benchmarks must be tied to a pro-forma Profit and Loss Statement (P&L) that indicates the level of return the portfolio will achieve.

Minimum components of benchmarks include:

What happens when a benchmark is breached?

When breached, corrective action is required to align performance with expectations.

Remedial actions can include:

Results of benchmark performance are part of the Balanced Scorecard process detailed in the RCR Credit Performance Management Standard.

Balanced Scorecard reporting is required for all non-liquidating retail lending portfolios with ENR of $50 million or more.

Three sets of acquisition benchmarks are assessed in the Balanced Scorecard each quarter: mix, early delinquency and losses

To proceed, select each benchmark to learn more.

Through-the-Door Mix

Quarterly performance measurement comparing actual booking profiles against mix guardrails/triggers set in the PRAP.

Early Delinquency by Vintage

Coincident delinquency for revolving products and ever delinquency for closed-end loans measured by vintage.

Losses (NCL/GCL) by Vintage

Gross Credit Loss (GCL) or Net Credit Loss (NCL) by vintage.

Retail businesses must maintain an inventory of all products and assess the risk profile of each product across all risk types. The credit risk rating for Retail products is called the Product Credit Risk Rating (PCRR).

You’ll find details about the required process, methodology and calculations in the Portfolio Monitoring and Categorization and Product Credit Risk Rating Standard.

To proceed, select each area to learn more about what's involved in the PCRR process.

The PCRR is based on the same three PMAC pillars used to categorize retail portfolios:

go to next button

Products are risk rated as High/Medium/Low based on PMAC categorization types:

go to next button

Citi uses a Lines of Defense (LOD) model to manage risk. Roles and responsibilities are grouped according to these LODs.

Within the Retail Credit Risk Management (RCRM) framework there are key credit roles in 1LOD and 2LOD that are responsible for the management and oversight of retail portfolios.

To proceed, select each key credit role to discover more.

Senior Country/Business Risk Manager (SC/BRM)

The lead risk manager for the country or business (1LOD) is accountable for the retail credit risk of their respective portfolio(s) and for all risk management activities detailed in RCR Policy, Standards and Procedures.

Group Risk Director (GRD)

GRDs (2LOD) manage and provide oversight to SC/BRMs for their designated business or function. GRDs monitor the credit risk/reward balance and performance of retail portfolios.

Global Product/Function Oversight Director (GP/FOD)

GP/FODs (2LOD) are designated based on their expertise in a specific product or functional area and are primarily responsible for providing cross-business oversight and independent review and effective challenge.

USPB Chief Risk Officer (CRO)

The USPB CRO is a 2LOD role accountable for the credit risk performance of all retail credit portfolios and responsible for leading the global RCRM group.

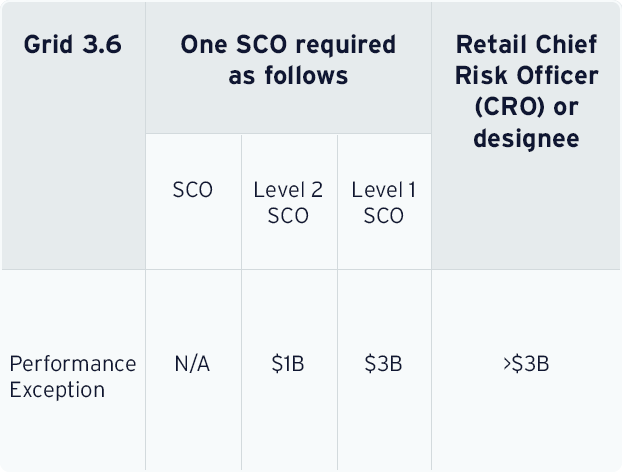

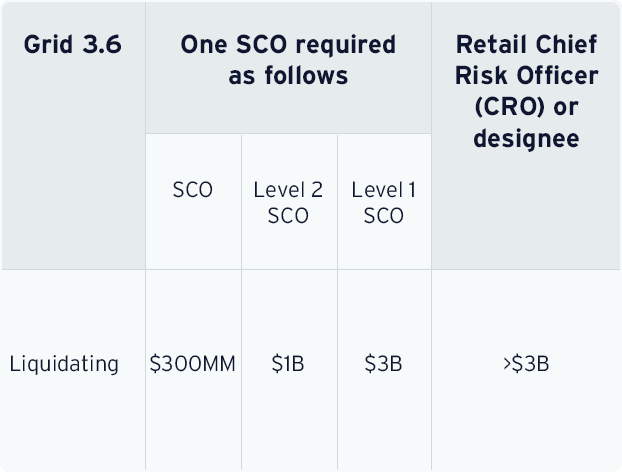

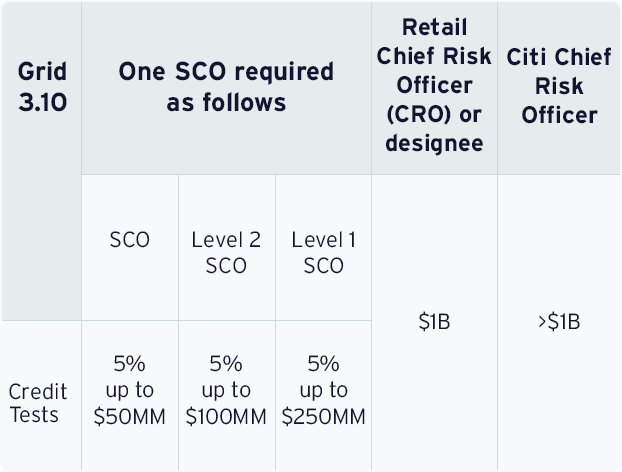

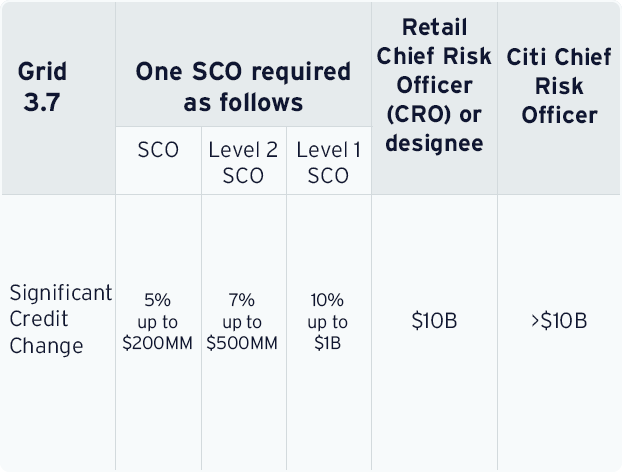

Each business must comply with requirements related to credit criteria, process and pricing exceptions outlined in RCR Credit Performance Management Policy (RCR Chapter 2) and the RCR Credit Performance Management Standard.

To learn more about each of these exception types, select each type of exception for a brief definition.

Credit Criteria Exceptions

Deviations to approved risk acceptance credit criteria including, but not limited to, credit score overrides, exceptions to debt burden, loan to value, minimum income, etc.

Process Exceptions

Deviations to approved policies and procedures regarding how information is obtained/verified or how the identity of an applicant is verified.

Pricing Exceptions

Deviations to published interest rates or fees.

The Quality Assurance Framework (QAF) provides a standardized risk control and assessment framework for all Retail portfolios across each phase of the Credit Risk Life Cycle. It ensures that In-Business processes throughout the life cycle are executed consistently and includes proactive monitoring for self-identification of issues.

For more about the QAF, consider the frequently asked questions below and refer to the RCR Quality Assurance Framework Procedure.

Who uses the QAF?

All Retail businesses lending to consumers or managing retail consumer credit portfolios are required to execute QAF monitoring activities and must adhere to the RCR QAF Procedure.

What is the QAF Credit Risk Control Matrix (CRCM)?

The CRCM is the core content of the QAF assessment and defines key RCR Policy requirements and Independent Risk’s expectations on how controls of key risks inherent in retail credit processes are monitored and measured.

What is the QAF output?

The results of QAF execution, defect level and severity ratings are aggregated based on the number of monitoring activities to assign a QAF risk rating at the portfolio level.

Purpose

Benefits

Approach

SC/BRMs or their designees assess risks qualitatively and rate the eight following categories relevant to Retail credit risk:

With comprehensive MIS, risk teams can strategically manage risk, identify underperforming segments and take action to manage exposure.

If you want to know more about general MIS requirements, consider the below frequently asked questions and refer to the RCR MIS & Reporting Standard.

What should comprehensive MIS measure?

Comprehensive MIS must track and validate:

Which indicators should Retail businesses monitor?

The following indicators must be tracked and reported to the SC/BRM monthly and must be available upon request to the GRD, GP/FOD or their designees:

For more details, refer to the RCR MIS & Reporting Standard.

Why is MIS important?

Monitoring of portfolio, vintage and segment level MIS across the Retail Credit Life Cycle is important to identify emerging trends, underperforming segments and to provide the necessary insight for adjustment of credit criteria to optimize the risk-reward balance of the portfolio.

Both 1LOD and 2LOD must ensure that MIS they produce and the underlying data is timely and accurate.

Purpose of Loss Mitigation Programs

Loss mitigation programs are used to address changes in the customer’s ability to repay a loan according to the loan’s terms and conditions of the original loan.

Key Criteria for Loss Mitigation Programs

Loss mitigation programs must be developed to address the customer’s duration and severity of cash flow reduction so that treatments are aligned to the customer’s condition.

Loss mitigation programs require evaluation methods to determine the customer’s ability and willingness to pay.

Long-term Treatments

Long-term treatments are offered to customers before write-off and result in a change of terms (interest rate and/or tenor) that results in a payment reduction for greater than 12 months in duration.

Examples of long-term treatments include rewrites, loan modifications (also called Adjustment of Terms), settlements, short-sales (applicable to real estate) and paydowns.

Short-term Treatments

Short-term treatments result in a change of terms (interest rate and/or payment amount) for less than or equal to 12 months in duration. In all cases, the minimum months on books for the loans treated in this manner is nine months.

Examples of short-term treatments include interest/fee waiver, payment reduction programs, extensions and deferments.

Phases one and two of the Retail Credit Life Cycle are Product Planning and Acquisitions. What are phases three and four?

Select the best response from the four options and then select Submit.

Please use the Space key only when selecting a radio option with the keyboard. The Enter key is not fully supported. If the Enter key has been used to select a radio option, please use the Escape key. Then you will be able to use the Space key again to select a radio option.

The Retail Credit Life Cycle consists of four important phases: Product Planning, Credit Acquisition, ECM and Collections & Loss Mitigation. The linkage of all phases to each other and continuous monitoring of retail portfolios throughout the Credit Life Cycle are critical to ensure retail lending activities are within the approved risk appetite.

Refer to Portfolio Governance, Retail Credit Life Cycle for more information.

Refer to Portfolio Governance, Retail Credit Life Cycle for more information.

That answer is correct.

That answer is not correct.

Refer to Portfolio Governance, Retail Credit Life Cycle for more information.

That answer is not correct.

Refer to Portfolio Governance, Retail Credit Life Cycle for more information.

That answer is not correct.

Refer to Portfolio Governance, Retail Credit Life Cycle for more information.

That answer is not correct.

Refer to Portfolio Governance, Retail Credit Life Cycle for more information.

That answer is not correct.

Refer to Portfolio Governance, Retail Credit Life Cycle for more information.

That answer is correct.

Which mechanism for documenting the credit risk management approach across the credit life cycle must include amongst its components, target market and focus statement, return and loss targets, profit and loss statements (P&Ls) and Key Risk Indicators (KRIs)?

Select the best response from the four options and then select Submit.

Please use the Space key only when selecting a radio option with the keyboard. The Enter key is not fully supported. If the Enter key has been used to select a radio option, please use the Escape key. Then you will be able to use the Space key again to select a radio option.

PRAPs document the credit risk management approach for retail portfolios across the full credit risk life cycle: product planning, acquisitions, ECM, collections and default management.

Refer to Portfolio Governance, Portfolio Risk Appetite Program for more information.

Refer to Portfolio Governance, Portfolio Risk Appetite Program for more information.

That answer is correct.

That answer is not correct.

Refer to Portfolio Governance, Portfolio Risk Appetite Program for more information.

That answer is not correct.

Refer to Portfolio Governance, Portfolio Risk Appetite Program for more information.

That answer is not correct.

Refer to Portfolio Governance, Portfolio Risk Appetite Program for more information.

That answer is correct.

That answer is not correct.

Refer to Portfolio Governance, Portfolio Risk Appetite Program for more information.

That answer is not correct.

Refer to Portfolio Governance, Portfolio Risk Appetite Program for more information.

What forward-looking risk management tool enables the business to prepare for upcoming stress and is based on establishing triggers, credit tightening actions, operational readiness, governance & communication and monitoring & execution?

Select the best response from the four options and then select Submit.

Please use the Space key only when selecting a radio option with the keyboard. The Enter key is not fully supported. If the Enter key has been used to select a radio option, please use the Escape key. Then you will be able to use the Space key again to select a radio option.

The Risks Readiness Playbook (RRP) enables the business to prepare for upcoming stress and is based on the five pillars listed in the question and triggers appropriate risk mitigating activities when defined leading indicators are tripped.

Refer to Portfolio Governance, The Five RRP Pillars for more information.

Refer to Portfolio Governance, The Five RRP Pillars for more information.

That answer is correct.

That answer is not correct.

Refer to Portfolio Governance, The Five RRP Pillars for more information.

That answer is not correct.

Refer to Portfolio Governance, The Five RRP Pillars for more information.

That answer is not correct.

Refer to Portfolio Governance, The Five RRP Pillars for more information.

That answer is not correct.

Refer to Portfolio Governance, The Five RRP Pillars for more information.

That answer is not correct.

Refer to Portfolio Governance, The Five RRP Pillars for more information.

That answer is correct.

All items below are key elements of Retail Credit Risk performance monitoring and portfolio management. Which one requires that Retail businesses maintain an inventory of all products and assess the risk profile of each product across all risk stripes?

Select the best response from the four options and then select Submit.

Please use the Space key only when selecting a radio option with the keyboard. The Enter key is not fully supported. If the Enter key has been used to select a radio option, please use the Escape key. Then you will be able to use the Space key again to select a radio option.

The Product Credit Risk Rating (PCRR) process is used to assess the risk profile of each product. PCRR is based on the same three PMAC pillars used to categorize retail portfolios as either PE, M&S or M&SW: Governance and Control, Credit Risk and Profitability Resiliency.

Refer to Portfolio & Product Performance Monitoring, Product Credit Risk Rating for more information.

Refer to Portfolio Governance, The Five RRP Pillars for more information.

That answer is correct.

That answer is not correct.

Refer to Portfolio & Product Performance Monitoring, Product Credit Risk Rating for more information.

That answer is not correct.

Refer to Portfolio & Product Performance Monitoring, Product Credit Risk Rating for more information.

That answer is not correct.

Refer to Portfolio & Product Performance Monitoring, Product Credit Risk Rating for more information.

That answer is not correct.

Refer to Portfolio & Product Performance Monitoring, Product Credit Risk Rating for more information.

That answer is not correct.

Refer to Portfolio & Product Performance Monitoring, Product Credit Risk Rating for more information.

That answer is correct.

Who is the lead 1LOD Risk Manager accountable for managing their retail portfolios and ensuring that all risk management activities comply with RCR Policy, Standards and Procedures?

Select the best response from the four options and then select Submit.

Please use the Space key only when selecting a radio option with the keyboard. The Enter key is not fully supported. If the Enter key has been used to select a radio option, please use the Escape key. Then you will be able to use the Space key again to select a radio option.

The Senior Country/Business Risk Manager (SC/BRM), as the lead Risk Manager for the country or business, is accountable for all 1LOD risk management activities detailed in the Retail Credit Risk Policy.

Refer to Credit Authority and Approval Rules, Credit Authority Roles for more information.

Refer to Credit Authority and Approval Rules, Credit Authority Roles for more information.

That answer is correct.

That answer is not correct.

Refer to Credit Authority and Approval Rules, Credit Authority Roles for more information.

That answer is not correct.

Refer to Credit Authority and Approval Rules, Credit Authority Roles for more information.

That answer is correct.

That answer is not correct.

Refer to Credit Authority and Approval Rules, Credit Authority Roles for more information.

That answer is not correct.

Refer to Credit Authority and Approval Rules, Credit Authority Roles for more information.

That answer is not correct.

Refer to Credit Authority and Approval Rules, Credit Authority Roles for more information.

Which type of exceptions are subject to quarterly RCR Policy exception limits?

Select the best response from the four options and then select Submit.

Please use the Space key only when selecting a radio option with the keyboard. The Enter key is not fully supported. If the Enter key has been used to select a radio option, please use the Escape key. Then you will be able to use the Space key again to select a radio option.

RCR Policy quarterly exception limits apply to credit criteria, pricing and process exceptions.

Refer to Retail Limits, Monitoring and Controls, Exception Limits for more information.

Refer to Retail Limits, Monitoring and Controls, Exception Limits for more information.

That answer is correct.

That answer is not correct.

Refer to Retail Limits, Monitoring and Controls, Exception Limits for more information.

That answer is not correct.

Refer to Retail Limits, Monitoring and Controls, Exception Limits for more information.

That answer is not correct.

Refer to Retail Limits, Monitoring and Controls, Exception Limits for more information.

That answer is not correct.

Refer to Retail Limits, Monitoring and Controls, Exception Limits for more information.

That answer is correct.

That answer is not correct.

Refer to Retail Limits, Monitoring and Controls, Exception Limits for more information.

Which one of the following ensures consistent execution of In-Business processes throughout the credit life cycle and includes proactive monitoring for self-identification of issues?

Select the best response from the four options and then select Submit.

Please use the Space key only when selecting a radio option with the keyboard. The Enter key is not fully supported. If the Enter key has been used to select a radio option, please use the Escape key. Then you will be able to use the Space key again to select a radio option.

The Quality Assurance Framework QAF ensures that In-Business processes throughout the credit cycle are executed consistently. It includes execution of monitoring activities to proactively monitor for self-identification of issues.

Refer to Retail Limits, Monitoring and Controls, Quality Assurance Framework (QAF) for more information.

Refer to Retail Limits, Monitoring and Controls, Quality Assurance Framework (QAF) for more information.

That answer is correct.

That answer is not correct.

Refer to Retail Limits, Monitoring and Controls, Quality Assurance Framework (QAF) for more information.

That answer is not correct.

Refer to Retail Limits, Monitoring and Controls, Quality Assurance Framework (QAF) for more information.

That answer is not correct.

Refer to Retail Limits, Monitoring and Controls, Quality Assurance Framework (QAF) for more information.

That answer is not correct.

Refer to Retail Limits, Monitoring and Controls, Quality Assurance Framework (QAF) for more information.

That answer is correct.

That answer is not correct.

Refer to Retail Limits, Monitoring and Controls, Quality Assurance Framework (QAF) for more information.

The importance of identifying emerging trends, underperforming segments and providing the necessary insight for adjustment of credit criteria to optimize the risk-reward balance of the portfolio is best accomplished through which of the following?

Select the best response from the four options and then select Submit.

Please use the Space key only when selecting a radio option with the keyboard. The Enter key is not fully supported. If the Enter key has been used to select a radio option, please use the Escape key. Then you will be able to use the Space key again to select a radio option.

Monitoring of portfolio, vintage and segment level MIS across the Retail Credit Life Cycle is important to identify emerging trends, underperforming segments and to provide the necessary insight for adjustment of credit criteria to optimize the risk-reward balance of the portfolio.

Refer to Management Information System (MIS), MIS General Requirements for more information.

Refer to Management Information System (MIS), MIS General Requirements for more information.

That answer is correct.

That answer is not correct.

Refer to Management Information System (MIS), MIS General Requirements for more information.

That answer is not correct.

Refer to Management Information System (MIS), MIS General Requirements for more information.

That answer is not correct.

Refer to Management Information System (MIS), MIS General Requirements for more information.

That answer is not correct.

Refer to Management Information System (MIS), MIS General Requirements for more information.

That answer is not correct.

Refer to Management Information System (MIS), MIS General Requirements for more information.

That answer is correct.

Which of the following is an example of a short-term loss mitigation treatment offered to a customer that would help address the customers difficulty repaying the loan?

Select the best response from the four options and then select Submit.

Please use the Space key only when selecting a radio option with the keyboard. The Enter key is not fully supported. If the Enter key has been used to select a radio option, please use the Escape key. Then you will be able to use the Space key again to select a radio option.

Loss Mitigation treatments are used to assist customers that have difficulty repaying the loan. Short-term treatments are offered to pre-write off customers and result in a change of terms for less than or equal to 12 months in duration. Examples of short-term treatments include interest/fee waivers, payment reduction programs, extensions and deferments.

Refer to Collections & Loss Mitigation, Loss Mitigation & Loss Recognition for more information.

Refer to Collections & Loss Mitigation, Loss Mitigation & Loss Recognition for more information.

That answer is correct.

That answer is not correct.

Refer to Collections & Loss Mitigation, Loss Mitigation & Loss Recognition for more information.

That answer is not correct.

Refer to Collections & Loss Mitigation, Loss Mitigation & Loss Recognition for more information.

That answer is not correct.

Refer to Collections & Loss Mitigation, Loss Mitigation & Loss Recognition for more information.

That answer is correct.

That answer is not correct.

Refer to Collections & Loss Mitigation, Loss Mitigation & Loss Recognition for more information.

That answer is not correct.

Refer to Collections & Loss Mitigation, Loss Mitigation & Loss Recognition for more information.

The Global Retail Lending Principles are the foundational elements of our risk appetite and culture for all lending decisions. Which one of the below is NOT one of the Global Retail Lending Principles?

Select the best response from the four options and then select Submit.

Please use the Space key only when selecting a radio option with the keyboard. The Enter key is not fully supported. If the Enter key has been used to select a radio option, please use the Escape key. Then you will be able to use the Space key again to select a radio option.

The Global Retail Lending Principles include 1) Treating customers fairly 2) Strategically aligning the product purpose, value proposition and credit policy 3) More underwriting scrutiny applies to customers without credit experience or significant negative history, and 4) Payment for the risk we take.

Refer to Portfolio Governance, Global Retail Lending Principles for more information.

Refer to Portfolio Governance, Global Retail Lending Principles for more information.

That answer is correct.

That answer is not correct.

Refer to Portfolio Governance, Global Retail Lending Principles for more information.

That answer is not correct.

Refer to Portfolio Governance, Global Retail Lending Principles for more information.

That answer is not correct.

Refer to Portfolio Governance, Global Retail Lending Principles for more information.

That answer is correct.

That answer is not correct.

Refer to Portfolio Governance, Global Retail Lending Principles for more information.

That answer is not correct.

Refer to Portfolio Governance, Global Retail Lending Principles for more information.

go to close menu button

go to close button